The previous era of moderate inflation and low interest rates has rapidly given way to a new era of macro and financial market volatility. Major asset classes have hit the reset button and investors across the board have pulled back.

The transition to a new world calls for a different asset allocation mindset with a sharper sense of the suite of risks likely to dictate the investment landscape.

The cyclical and structural case for investing in the private market alternative of real estate credit is strong. As part of a diversified portfolio, it offers reliable and inflation-adjusted income return. Equally important is the defensive strength and clear line of sight for downside capital protection provided by the security attached to its underlying investment – the first ranking mortgage.

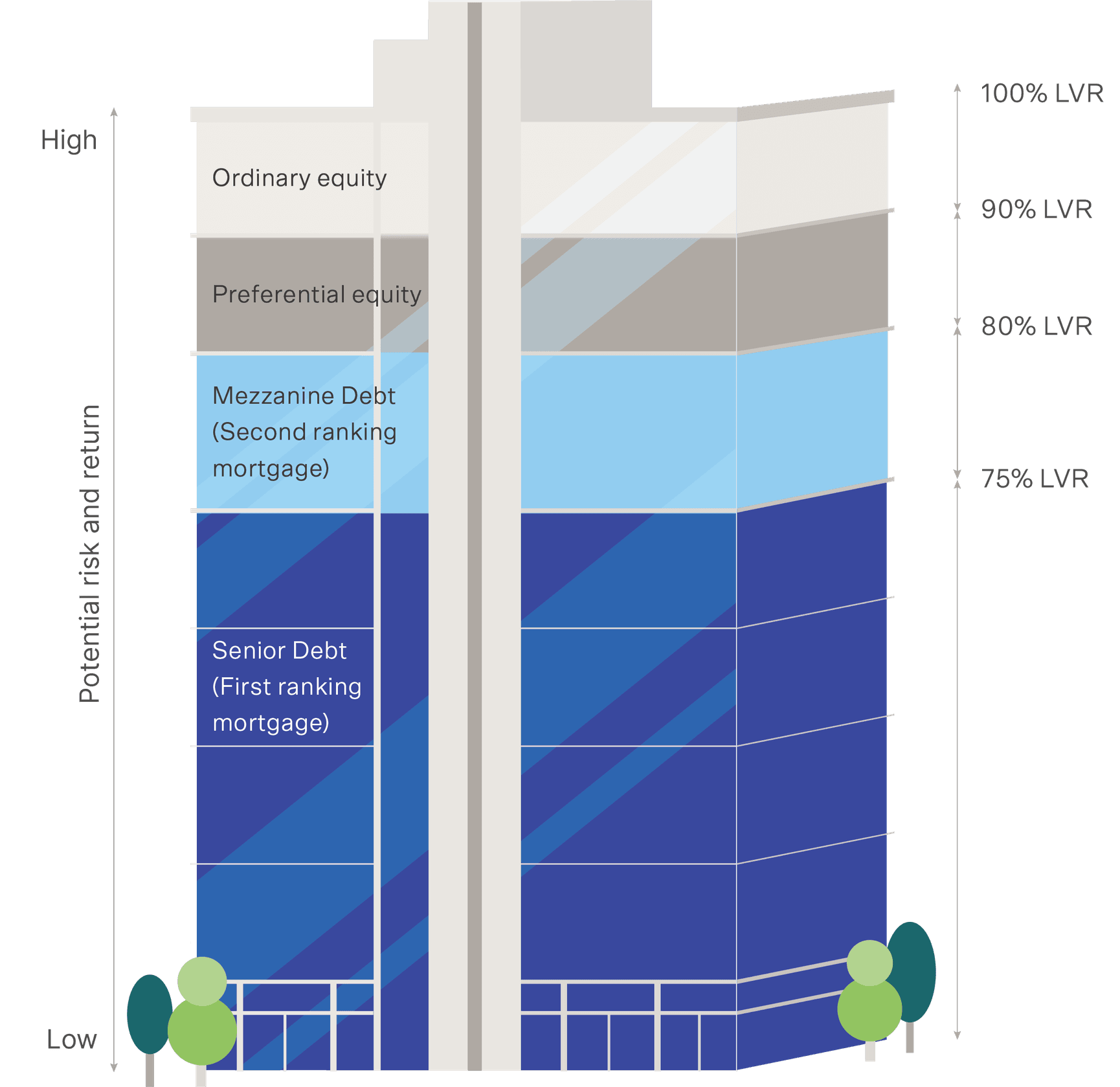

Real estate credit capital tower

Critical in understanding the strength of the downside capital protection real estate credit delivers is the underlying mix of equity and debt used to finance an asset – its capital structure.

Think of the capital structure as a building, with the riskiest position at the top, and the least risky and most stable at the bottom of the building.

Equity holders occupy the top-end of the tower – the riskiest position.

Ordinary equity sponsors manage or control the asset/entity in what is known as the ‘first-loss’ position. An income return, or dividend, is not guaranteed and if the saleable value of the asset decreases, equity funds are the first to be reduced or lost.

Next floor down in the risk/return pillar is preference equity. Installed at the discretion of the sponsor’s partners or syndicate of lenders, this debt/equity hybrid is an optional level that is generally paid a fixed percentage of dividends payable. It sits in a ‘second-loss’ spot after ordinary equity holders.

The capital foundation | First-ranked mortgages

Further down the risk capital tower is the debt (or real estate credit) foundation.

Topping the debt base is ‘mezzanine debt’, usually secured by a second ranking mortgage over the asset and positioned above any equity holders in repayment.

Real estate credit issued as ‘senior debt’, secured by a first-ranking mortgage over the asset, occupies the solid, stable, and safest location within the capital tower. The position gives the lender (investor) the right to repayment from the value of the asset ahead of any other creditor or the borrower.

Critically, a registered first ranking mortgage also gives the lender the right to control the property if the borrower defaults. In the hands of an experienced manager, this added security ensures lender’s (investor’s) capital can be managed prudently if the loan covenants are breached.

Typically, real estate credit loans are relatively short in duration, the maximum loan term is generally 24 months. The shorter-term loan reduces exposure to individual borrowers, sectors or securities and cyclical movements and also ensures the initial due diligence remains relatively current, providing a further protection against capital loss.

Weathering the storm

Population estimates indicate Australia may experience growth rates of up to 1.4% p.a. by 2024-25, outpacing many regions in the developed world.1 Population growth helps create a balance between labour demand and supply, contributing to a stable, growing economy.2 Increasing activity in the credit (debt) sector of the capital stack will be necessary to fund critical housing and real estate development.

Additionally, as financial markets remain highly volatile investors may look to secure an increasingly defensive capital position. The underlying asset in real estate credit (the first-ranked mortgage) is not the only protection offered from the turbulent conditions ahead. Shorter-duration loans (maximum of two years) and low loan-to-value ratios (LVR) combine to further bolster the defensive shield in the event of declining value in the underlying asset.

Accessing real estate credit

An expanding suite of real estate credit investment products are available in Australia.

Accessing real estate credit is open to institutional, wholesale and retail investors through open and closed-end funds, bespoke mandates, partnerships, and separately managed accounts.

Diversified funds typically employ open-ended structures. With a minimal initial investment, open-ended real estate credit funds allow investors in and out of the fund during its life. Distributions are paid on a regular, typically monthly or quarterly, basis and target returns can be linked to official interest rates in line with a floating rate structured loan portfolio. Investments are selected and held at the discretion of the manager.

Real estate credit provides a defensive investment with regular income and low downside capital risk through the security and control attached to the structure of the underlying investment, the first ranked mortgage.

This insight is the first in our Real Estate Credit Investment Series, to view the full series please click here. For more information about our real estate credit capabilities and solutions, please get in touch.

1. Australian Government Centre for Population, 2022-23 Budget: Australia’s Future Population, www.population.gov.au

2. The determinants of Australia’s future demography, Peter McDonald, Australian National University, www.pc.gov.au

Important Information: This material has been prepared by MA Asset Management Ltd (ACN 142 008 535) (AFSL 327 515). The material is for general information purposes and must not be construed as investment advice. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer or invitation to purchase, sell or subscribe for in interests in any type of investment product or service. This material does not take into account your investment objectives, financial situation or particular needs. You should read and consider any relevant offer documentation applicable to any investment product or service and consider obtaining professional investment advice tailored to your specific circumstances before making any investment decision. Any investment in a fund managed by MA Financial Group is subject to the terms and conditions of the relevant fund offer document. This material and the information contained within it may not be reproduced or disclosed, in whole or in part, without the prior written consent of MA Asset Management Ltd. Any trademarks, logos, and service marks contained herein may be the registered and unregistered trademarks of their respective owners.

Nothing contained herein should be construed as granting by implication, or otherwise, any licence or right to use any trademark displayed without the written permission of the owner. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of MA Asset Management Ltd. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Additionally, this material may contain “forward-looking statements”. Actual events or results or the actual performance of MA Asset Management Ltd or an MA Asset Management Ltd financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. Certain economic, market or company information contained herein has been obtained from published sources prepared by third parties. While such sources are believed to be reliable, neither MA Asset Management Ltd, MA Financial Group or any of its respective officers or employees assumes any responsibility for the accuracy or completeness of such information. No person, including MA Asset Management Ltd and MA Financial Group, has any responsibility to update any of the information provided in this material.